ENERGIZED: Investment Insights on Energy Transformation

Edition 5

The Electrification Supercycle: Equipment Opportunities

18 March 2025

Please note: This newsletter is for general informational purposes only and should not be construed as financial, legal or tax advice nor as an invitation or inducement to engage in any specific investment activity, nor to address the specific personal requirements of any readers. (Full disclaimer below).

Key Takeaways:

Electrification will be an energy megatrend, as transport, heating, cooling, industry and storage shift from traditional to electric solutions, bringing more secure, efficient and cleaner energy consumption

The historic grid overhaul required to keep pace with renewable capacity expansion means investing in up to 80m km of transmission and distribution (T&D) infrastructure

Critical equipment supply chains are already very stretched: cables, transformers, converters, switchgear, circuit breakers, capacitors and control equipment

Multi-year order backlogs and rapid price inflation put existing suppliers in a strong position, but recent anti-transition sentiment seems to have impacted share prices

Denmark’s NKT is one well-placed specialist in the fast-growing high-voltage (HVDC) cable segment - using its strong cash flow to expand capacity and extend its very healthy pipeline for offshore wind farm connections and interconnectors

Risks to expected T&D / HVDC demand growth involve a combination of demand side flexibility, location optimisation, grid enhancing technologies, energy efficiency, AI, battery storage growth and market design changes.

Disclosure: At the time of publication, none of the companies mentioned in this edition are part of the Energized portfolio.

The Next Supercycle

In the early years of this century, China’s rapid growth drove a commodity “supercycle”. As new supply struggled to keep pace with demand, this rising tide lifted oil and gas prices and the industries and infrastructure behind them.

The next energy supercycle could well be electrification. Much analysis tends to focus on the relative share of electricity supply sources, but that’s only one part of a much bigger picture. Electrification is a more fundamental question: what proportion of total final energy demand is consumed as electricity, rather than other fuels like gas, petrol, diesel and coal. (The same term also refers to the level of electricity access among populations).

At only just over 20% globally, there’s plenty of room for growth. China, the world’s “electric superpower”, is closing in on 30%, far ahead of the US and Europe on 22% and 21% respectively. Current policies would see global electrification reach 28% (i.e. around China’s current level) by 2050. By contrast, the hypothetical Net Zero scenario limiting global warming to 1.5ºc would require over 50% by that year. So even if we don’t “electrify everything”, the electrification megatrend – however fast it happens – will be a profound shift in humanity’s relationship with energy: making it more efficient, more secure, cleaner and healthier.

Source: Enerdata

Powering Up

Electrification rates in the western world have been sluggish in recent years but are expected to accelerate as we enter a new phase of higher power demand growth. After last year’s 4.3%, the International Energy Agency (IEA) expects global power demand growth to continue at similar rates over the next few years. AI, data centres and crypto mining often grab all the headlines, but there are several fundamental drivers:

Electrification of transport: from ICE to electric vehicles (from motorbikes to cars to trucks) and associated infrastructure (petrol stations to charging stations)

Electrification of building heating, cooling and management: from gas boilers to heat pumps, air conditioning, controls

Electrification of industry: from coal and gas fired to electrically powered factories, industrial processes and appliances

Electrification of energy storage: from pumped hydro to batteries

Electrification needs transmission

The phrase “no transition without transmission” is so true that it has become an energy cliché. Meeting this new wave of new power demand means transforming energy infrastructure: not only rapid renewable capacity expansion but also the transmission and distribution lines to deliver it to consumers. The grid is sometimes referred to as the world’s largest machine, or the veins of the world’s energy system. It is in many ways a modern miracle, but it has its work cut out to avoid becoming a bottleneck on human progress.

As renewable capacity additions rise further, from 666 GW in 2024 to towards the 1 TW (1000 GW or 1 million MW) mark by around 2030, this grid overhaul becomes ever more urgent. 1.65 terawatts of advanced stage renewable projects have been identified as awaiting grid connections – that’s more than the total installed utility-scale electricity generation capacity of the US. The IEA reckons 80 million km of lines (200 times to the moon and back) need to be built or refurbished over the next 15 years, at a cost of $200-300 billion per year by 2035.

It is not just about sustainability and clean power. Regardless of generation source, building and integrating strong grids enhances resilience and security. In a more digitised and AI-oriented world, they become the cornerstone of growth, prosperity and competitiveness. A gas-import dependent region like Europe has a compelling strategic interest in maximising its use of self-generated power.

Grid investment: stepping up

Historically, grid investments have been a tough sell for governments and investors, being highly capital intensive, low-return and long-term in payoff. Demand side growth wasn’t strong enough to justify building ahead. High degrees of certainty were required for such large capital commitments.

With the structural upturn in power demand, that is now changing. Over this decade, Rystad Energy projects annual grid investment to triple from ~$50bn to ~$150bn in China, double from ~$50bn to ~$100bn in both the US and Europe respectively, and double from ~$75bn to ~$150bn in the rest of the world, implying total global grid investment of ~$600bn by 2030.

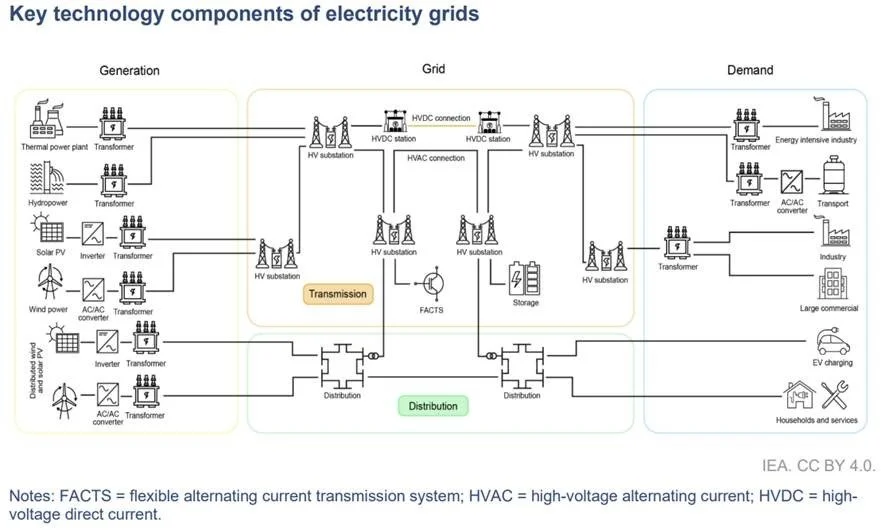

Critical equipment bottlenecks

The grid buildout race means not only more regional and national transmission lines, but also subsea interconnectors and high-voltage cables connecting offshore wind farms into grids. A significant growth area is high and ultra-high voltage direct current (HVDC and UHVDC) long-distance systems, especially in bigger countries like China where renewable power can be generated far from big cities. Then there is the need to connecting grid-scale battery systems (BESS) into grids.

This accelerating grid buildout has created a rush for critical electrical equipment, including:

Cables – low-, medium- and high-voltage depending on the application

Transformers – used to step voltage up or down, e.g. at substations

Converters – used to switch between alternating current (AC) and direct current (DC) systems

Switchgear and circuit breakers – used to control and isolate electrical equipment, protecting from overloads and faults

Capacitors and supercapacitors – used to stabilise voltage and power output by blocking DC currents while allowing AC to flow

Control equipment

Are current shortages just a foretaste of what’s to come in the electrification supercycle? Assessing where we are in the cycle of shortage versus new capacity is a complex puzzle. What we do know is that rising competition has extended order backlogs to 2-3 years in several categories – and even to 4-5 years in some cases. Inevitably this has triggered cost inflation, with prices of some equipment nearly doubling since 2019. Further complexity arises from the need for customisation: rather than being modular, off-the-shelf solutions, much electrical equipment must be manufactured specifically for each unique application. They also each have complex supply chains of their own.

Source: IEA

European suppliers

So which equipment supply companies stand to gain most from the long-term growth in power demand? The European contenders include some names you may have heard of but many probably haven’t:

Prysmian (Italy, up 85% over the past 3 years)

Nexans (France, 14%)

NKT (Denmark, 89%)

Schneider Electric (France, 53%)

Rexel (France, 28%)

Siemens Energy (Germany, 184%)

ABB Ltd (Switzerland, 72%)

Legrand SA (France, 16%)

Some of these are more general engineering and supply companies, while others are specialists. As previously noted, power equipment suppliers like Siemens and Schneider have already risen substantially as beneficiaries of the AI investment trend. There’s a lot of ground to cover here, so for now let’s zoom in on the cable segment and look at one company on this list that seems well positioned: Denmark’s NKT.

The cable guys

Founded in 1891, NKT is a pure-play cable provider, manufacturing low-, medium- and high-voltage power cables and associated equipment mainly for the European market. Several years of strong growth have lifted its market value close to £3bn. Following ~€4bn of contract awards over the past 2 years, NKT now a has high-voltage order backlog of over €10bn, plus another €3.5bn of capacity reservations. That translates into full capacity utilisation and strong earnings visibility over the rest of this decade.

Cables are clearly an essential ingredient in grid expansion and NKT has built a strong niche in the high-voltage category which looks set to remain the most stretched part of the market. These are typically used for longer-distance transmission such as interconnectors and linking offshore wind farms to onshore grids. An estimated ~€10bn/pa addressable high-voltage cable market out to at least 2030 leaves NKT well placed to pick up further contract awards. Just last week, the UK’s National Grid awarded two parts of a £59bn HVDC supply chain framework to a group of suppliers including NKT.

Interconnectors: a growing market

Interconnectors are high-capacity transmission lines that transfer large amounts of power across borders (and seas) to high-demand areas. As Europe shifts to a more electrified economy, they are strategically significant assets playing a critical role in energy security. Proposed projects are getting ever more ambitious: notably the Morocco-UK X-Links project and even a US-Europe link being discussed.

The UK already has 10 interconnectors importing from five different countries (France, Norway, Denmark, Belgium and the Netherlands) and exporting to Ireland, demonstrating their essential role. Those lines collectively provide on average around 12-14% of UK power supply, and there are several more either planned or already being developed as the UK’s power consumption expected to more than double by 2050. These will include “Offshore Hybrid Assets”, the next generation of interconnector which will integrate with offshore wind farms, such as the planned Netherlands-UK LionLink.

Major domestic transmission lines are likewise vital to avoid large amounts of stranded power. The 2 GW Suedlink line, which NKT is supplying, is a big deal for Germany as it will connect the north, where most wind power is generated, with major demand centres in the south. Similarly, in the UK, National Grid’s “Great Grid Upgrade” features 17 major infrastructure projects including new north-south transmission lines and links to gigascale offshore wind farms.

NKT has a strong track record of supplying major European interconnectors, including:

Viking: Denmark-UK, 1.4 GW, 525 kV DC (world’s longest land and subsea power cable)

NordLink: Norway-Germany, 1.4 GW, 525 kV DC

BritNed: Netherlands-UK, 1 GW, 450 kV DC

Korridor-B: Denmark-Germany, 2 GW, 525 kV DC

NorNed: Norway-Netherlands, 0.7 GW, 450 kV DC

NordBalt: Sweden-Lithuania, 0.7 GW, 300 kv DC

EWIP: UK-Ireland, 0.5 GW, 200 kV DC

Estlink: Finland-Estonia, 0.35 GW, 150 kv DC

This transmission map gives an idea of the ever more complex web of grid interconnectivity across north west Europe.

Source: ENTSO-E

Financial growth

It’s therefore no surprise that NKT has seen very strong growth in recent years. Annual revenues grew 25% in 2024 to reach €3.25bn, compared to €1.83bn only 3 years earlier. Operational income rose 35%, net income nearly tripled to €337m and free cash flow was also up nearly a third to €400m, leaving it with ~€1.3bn in liquidity. It’s return on capital employed (ROCE), which measures the efficiency of its investments, also rose from 20% to 35%.

Company guidance for 2025 is cautious, projecting revenues and operating income at similar levels to its record year in 2024, given there will be no new capacity yet online to exploit prevailing market tightness. However, it has upgraded its 4-year financial outlook to:

Organic revenue growth rate 2021-28: >14% (previously 12%)

Projected 2028 EBITDA: €700m by 2028 (previously €550m)

Projected 2028 Return on Capital Employed: 20% (no change)

Scaling up

Naturally, NKT is investing in extra capacity to take advantage of especially high demand in the HVDC space: expanding its manufacturing facility in Karlskrona, Sweden, and commissioning a second cable-laying vessel to boost its offshore installation capabilities.

These investments mean higher expenditure for NKT over 2025-26, especially as some cost inflation has crept in. But they should leave it very well equipped to compete for global opportunities beyond its traditional European backyard. On completion in 2027, Karlskrona will be the world’s largest high-voltage offshore cable production site.

A reasonable entry point?

After hitting an all-time high of DKK 667 in mid-September 2024, NKT shares fell steadily over the next 5 months to DKK 451 by early February. This 32% drop doesn’t seem justified by the fundamentals. Deteriorating market sentiment on the energy transition is almost certainly a factor. The G&P Global Clean Energy index fell around 24% over the same period.

This recent pullback may provide a sensible long-term entry opportunity. Since early February, it has already started recovering, reaching DKK 525 at the time of writing, although that’s still around 20% below its September 2024 peak. Earnings per share (EPS) have risen strongly in line with business growth over the past 4 years, nearly doubling from €2.16 in 2023 to €4.21 in 2024.

At a current Price/Earnings ratio of 16.6x NKT may not be particularly undervalued. If operating income doubles again over the next 4 years to €700m as NKT projects, that multiple implies a share price of DKK 765-775 by 2028. That would be 46% total growth - or compound annual growth of ~10% - over that period. This healthy but not excessively ambitious level of appreciation seems fair given the industry tailwinds - it’s far lower than the 128% gain of the past 4 years.

With its strong balance sheet and project pipeline, NKT may therefore be one reasonable long-term way to get exposure to the high demand for HVDC transmission on the road to wider electrification. By that time, with its capacity expansion complete, it could also be well positioned to start returning capital via dividends while still being able to fund incremental organic growth.

Danger: high voltage!

As always, there are relevant counter arguments worth considering. The cost and time involved in building new gride infrastructure creates strong incentives for alternative solutions which could undercut the expected high growth in transmission, especially HVDC, demand. Expanding transmission is undoubtedly an essential part of the mix, but other routes to address global grid congestion include:

Demand side flexibility: Demand side response mechanisms have the potential to unlock significant latent slack in existing power systems, by shifting demand to better match supply.

Location optimisation: In future, more demand is expected to be located closer to renewable supply, positioning to take advantage of periods of oversupply when marginal costs can fall to zero or even negative. This could help to reduce the need for incremental transmission infrastructure.

Energy efficiency: Efficiency measures, if successfully raised from the current 1%/pa energy intensity improvement to the target 4%/pa level, could make power demand growth to turn out lower than expected. There is some historical precedent for this. Widespread concern about AI’s impact on power demand looks overdone, especially given the potential for leaps in AI efficiency (as DeepSeek’s emergence shows). That said, energy efficiency and electrification are hard to disentangle – they are often two sides of the same coin.

AI: Besides getting more efficient itself, AI and machine learning may also help accelerate efficiencies in power and other systems, thereby reducing demand.

Storage: Very rapid expansion in battery systems means more scope to store power, potentially mitigating the need to expand long-distance transmission capacity. BESS is increasingly co-located with new renewable capacity additions to ensure greater capacity usage.

Market design: Zonal pricing regimes could encourage more localised power consumption and reduce the need to transport it elsewhere.

Grid enhancing technologies: Software and hardware solutions that effectively expand the carrying capacity of existing grids in low-cost ways may also help to curtail the need for new capacity. These include dynamic line rating, dynamic transformer rating, topology optimisation, advanced conductor technology, power-flow control devices, and real-time data gathering tools including meters and sensors that can optimise capacity usage by up to 50% (probably for another whole edition in due course…).

Key commodities and indices

Moving on to current energy markets: one stat jumps out of the data below: at current exchange rates, the UK front month (April) power price is now three times its Spanish equivalent, versus ~1.65x a year ago. High UK power prices are often blamed on the increasing share of renewables in the mix. If that were true, you’d expect Spain to rely less on renewables, given its much lower prices. In fact, Spain’s share is higher than the UK (55.8% in 2024 vs 38.2% for the UK, or 45% if you include biomass, which is debatable).

In fact, Spain’s lower prices are driven by its much lower share of gas (only ~13%) in the mix. The other factor is greater diversification. Supply is fairly evenly distributed between wind (2024 average: 22.9%), nuclear (19.6%), solar (18.3%) and hydro (13%). By contrast, in the UK wind (30%) is far ahead of nuclear (14%), solar (5%) and hydro (2%), while gas (26.3%) has twice the share it has in Spain. (In 2022, during the European energy crisis, Spain and Portugal also temporarily capped the gas price used for power generation to protect consumers.)

Although solar is growing fastest in Spain, wind is currently the top single source in both countries, but the UK is already much more wind dependent. So when UK wind output is relatively low, the call on gas increases, which usually drives power prices up - or at least keeps them high. And in fact, over recent months lower wind speeds are exactly what has happened, along with a slightly colder winter, driving higher gas demand.

At the time of writing, the very sunny early afternoon of Tues 18 March, solar happens to be the largest single power source on the UK grid, at 27.3% / 10 GW, followed by wind on 24.5% and interconnectors on an unusually high 21.1%. At this moment, solar is producing twice as much as gas (13.8% / 5.0 GW), pushing current UK power emissions below the 100 g/kWh mark. Of course, a single moment is fairly irrelevant; what matters are averages over time. Zooming out to just the past week, the solar share falls to 5.3%, one eighth of gas on 42.1%. The UK’s power mix is going to change radically over the next 5 years, but there is a long way to go.

Even as renewables produce over 52% of UK power, the spot power price remains stubbornly high at £81.76 / MWh. The reason is that in practice, it is almost always set by gas prices as the marginal source of supply - even when like now it is only a fraction of the total picture. The UK now imports around half its gas consumption, as domestic production hit a 50 year low of 3 billion cubic feet per day in 2024. Given gas’ dominant role in heating, this import dependency is here to stay, even with a rapid uptake in heat pumps. So no matter where it is produced, the UK remains at the mercy of regional gas prices. The good news for consumers is that a cyclical gas market downturn looks likely over the next 1-3 years given expected supply growth - and geopolitics could yet accelerate that if a Ukraine peace deal is reached.

The UK was briefly a net power exporter when much of the French nuclear system chose a bad year to be offline during the European energy crisis. But in general, the UK imports 10-15% of its power, an amount that is steadily growing as European interconnection expands. If anything, that should help to reduce UK power prices, but the only realistic route to sustained lower power prices is that gas market crash, whenever it comes…

On that note, having reached a near two-year high on 10 February, front-month European gas prices cratered by a third over the following 4 weeks to 6 March, as speculative money cashed out. Sentiment turned sharply bearish with the first moves towards talks – if they can be called that – on the future of Ukraine as well as a change in expectations on the EU’s mandatory gas restocking targets. Front-month gas prices have since recovered slightly to sit currently very close to our predicted average 2025 level of €40/MWh / 100p/therm, but still down 16% year to date. Having risen for exactly a year off their February 2024 low until 10 February 2025, it would be no surprise if that date proves to be this year’s high point for European gas prices.

Important Disclaimer: This newsletter is for general informational purposes only and should not be construed as financial, legal or tax advice nor as an invitation or inducement to engage in any specific investment activity, nor to address the specific personal requirements of any readers. Any investments referred to in this newsletter may not be suitable for all investors. In reading this newsletter you acknowledge that it is your responsibility to ensure that you fully understand those investments and to seek your own independent professional advice as to the suitability of any such investment and all the risks involved before you enter into any transaction. Strome Partners accepts no liability for any loss or adverse consequences arising directly or indirectly from reading or listening to the materials herein and on our website and make no representation regarding accuracy or completeness. We accept no responsibility for the content or use of any linked websites and third-party resources. Future events are inherently uncertain and there can be no certainty that any assessments, projections, opinions or forward-looking statements provided or referred to herein will prove to be accurate.